- Save your money and get interest. Work to make money at the same time.

- Always have and work towards a financial goal. Adjust your goals as necessary but never abandon them.

- Begin a retirement and investment account now. The earlier you start a long term savings/investment account, the bigger the payoff in the future.

- If you don't have the CASH to pay for it, you can't afford it. Bring able to make the instalment payments doesn't mean you can afford it.

- Money isn't everything and greed is not good.

- Save at least 10% of each and every paycheque. Force yourself to do this. It will pay off in the LONG run.

- A sale in a store is not a sale if you can't afford it.

- Earn some, save some, spend some.

- Spend less than you earn.

- If your outflow exceeds your income, your upkeep will be downfall.

Monday, July 31, 2006

TOP 10 Money Rules

Saturday, July 01, 2006

June 2006 Market Review and Outlook

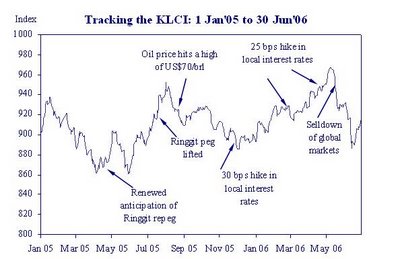

KLCI Continues to Ease with Regional Markets

Commencing the month at 930.4 points, the KLCI fell amidst continued declines in regional markets to its year low of 883.2 points in mid-June. However, a rebound in global and regional markets towards the end of June helped the KLCI to close at 914.7 points for a reduced loss of 1.4% for the month of June 2006.

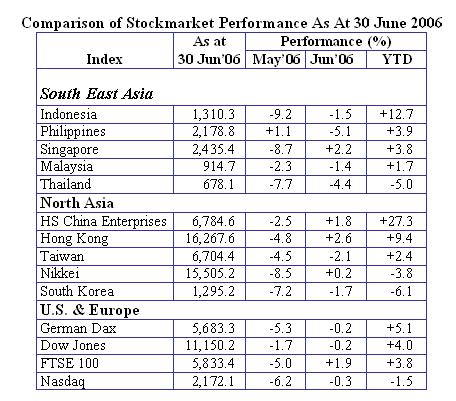

Regional markets closed on a mixed note as concerns of excessive tightening of U.S. monetary policy by the U.S. Federal Reserve diminished. A rebound on Wall Street caused selected regional markets to stem earlier losses in late June. South East Asian markets generally closed weaker while North Asian markets managed to register marginal gains in June.

On Wall Street, the Dow also eased to near its year low of 10,667.4 points in mid-June on concerns of further interest rate hikes before rebounding to 11,150.2 points, down by a marginal 0.2% for the month. The Nasdaq closed 0.3% lower at 2,172.1 points over the same period.

Commencing the month at 930.4 points, the KLCI fell amidst continued declines in regional markets to its year low of 883.2 points in mid-June. However, a rebound in global and regional markets towards the end of June helped the KLCI to close at 914.7 points for a reduced loss of 1.4% for the month of June 2006.

Regional markets closed on a mixed note as concerns of excessive tightening of U.S. monetary policy by the U.S. Federal Reserve diminished. A rebound on Wall Street caused selected regional markets to stem earlier losses in late June. South East Asian markets generally closed weaker while North Asian markets managed to register marginal gains in June.

On Wall Street, the Dow also eased to near its year low of 10,667.4 points in mid-June on concerns of further interest rate hikes before rebounding to 11,150.2 points, down by a marginal 0.2% for the month. The Nasdaq closed 0.3% lower at 2,172.1 points over the same period.

Malaysia’s export growth slowed to a 9-month low of 6.3% in April from 9.5% in March and 11.9% in 1Q2006 due to slower exports of electronic & electrical and commodity products. Likewise, import growth also eased to 11.4% in April from 14% in March on weaker imports of capital and consumption goods. As a result, Malaysia’s trade surplus narrowed to RM7.2bil in April from RM9.6bil in March. The cumulative trade surplus for the January to April 2006 period of RM33 bil is about the same level as the previous corresponding period in 2005.

Malaysia’s export growth slowed to a 9-month low of 6.3% in April from 9.5% in March and 11.9% in 1Q2006 due to slower exports of electronic & electrical and commodity products. Likewise, import growth also eased to 11.4% in April from 14% in March on weaker imports of capital and consumption goods. As a result, Malaysia’s trade surplus narrowed to RM7.2bil in April from RM9.6bil in March. The cumulative trade surplus for the January to April 2006 period of RM33 bil is about the same level as the previous corresponding period in 2005.Domestic demand remained resilient with consumer loans growth moderating slightly to 17% in May from 18.6% in April as demand for vehicle financing weakened amid uncertainty over the outlook for car prices. The banking system’s overall loans growth remained stable at 8.9% in May on the back of firm demand for corporate loans.

Malaysia’s foreign reserves rose by a bigger margin of RM10.5bil in May to RM289.5bil as at 31st May compared to an increase of RM7.4bil in April. The increase in reserves is attributable to higher repatriation of export earnings and net capital inflows.

The local inflation rate eased to 3.9% in May from 4.6% in April as transport costs rose at a slower pace of 12.4% in May compared to 16.9% in April. However, the inflation rate is expected to remain high in coming months following Tenaga’s hike in electricity rates with effect from 1st June.

On the international front, economic activities in the U.S. show signs of moderating with the U.S. durables goods order growing at the slowest pace in 10 months of 3.3% in May from 10.8% in April following a sharp fall in civilian aircraft orders. However, consumer confidence as measured by the Conference Board rebounded slightly to 105.7 in June from 104.7 in May due to expectations that the business outlook and the job market are likely to improve.

The U.S. inflation rate rose to a 7-month high of 4.2% in May from 3.5% in April due mainly to higher fuel prices while core inflation (excluding food and energy) edged up to a 15-month high of 2.4% from 2.3% over the same period.

The Federal Reserve raised the Federal funds rate for the 17th time by 25 basis points to a 5-year high of 5.25% at the FOMC meeting on 29th June. Although the Federal Reserve stated that economic growth is moderating from its strong pace earlier this year, it noted that some inflationary risks remain and the outlook for interest rate policy will depend on the incoming data.

On the currency front, the U.S. dollar strengthened by 2.8% against the Euro and 4% against the Yen respectively in June on expectations that U.S. interest rates will continue to exceed interest rates in Europe and Japan. The U.S. dollar also appreciated versus other regional currencies amid the recent correction in emerging markets. The Ringgit eased by 1.5% to RM3.69 against the U.S. dollar for the month. Meanwhile, oil prices moved in a trading range around the US$70/brl level in June before ending the month unchanged at US$71/brl.

Stockmarket Outlook

The sharp correction in global and regional financial markets in May and June was triggered by concerns that an overtightening of U.S. monetary policy by the U.S. Federal Reserve could lead to a sharper-than-expected slowdown in the global economy. After making 17th consecutive hikes in interest rates, the U.S. Federal Reserve may be reaching the end of its monetary tightening cycle with a potential pause in interest rates after another potential hike at the 8th August FOMC meeting.

Despite concerns over the effect of tighter monetary policies, global economic growth is still expected to be sustained at between 4% and 5.0% this year compared to 4.8% last year. The anticipated slowdown in U.S. economic growth could be mitigated by the current strengthening of the Japanese and Euroland economies while China continues to grow at a strong pace.

On the regional front, economic growth is expected to moderate in most Asian economies in 2H2006 as global demand for manufactured exports weakens in tandem with the anticipated slowdown in the U.S. economy. However, selected regional economies with a significant domestic sector may be able to mitigate any slowdown in the external environment. On the valuations front, the recent sell-down in regional markets has sufficiently discounted the risk of overtightening by the U.S. Federal Reserve as valuations of selected regional markets have reached fairly attractive levels.

On the local front, Bank Negara is expected to maintain a tightening stance on monetary policy to keep inflationary pressures under control and ensure that real interest rates remain positive. However, the anticipated hikes in domestic interest rates in 2H2006 are expected to be moderate given the prospect of a peaking in U.S. interest rates by August 2006 and the high levels of liquidity in the banking system.

Despite the challenging external environment, Bursa Securities is a defensive market underpinned by fair valuations and reasonably attractive dividend yields. Bursa Securities’ P/E rating of 14.7x 2006 earnings is 17% below the 7-year historical average (1999-2005) of 17.7x. The market is underpinned by a gross dividend yield of 4.5% which compares favorably to Ringgit fixed deposit rates for less than a year’s tenure.

Wednesday, March 29, 2006

Benefits of Investing in UNIT TRUST

Unit trust funds provide you with a simple, convenient and less time-consuming method of investing in securities compared to investing directly in the stock market or any other eligible market. As an investor you are able to benefit from the expertise of full-time professional fund managers without the need to worry about what kind of securities to buy and when to get in and out of the market. By investing in unit trust funds, you have the opportunity to spread your money over a diversified portfolio of assets which otherwise may not be possible on your own.

Unit trust funds provide you with a simple, convenient and less time-consuming method of investing in securities compared to investing directly in the stock market or any other eligible market. As an investor you are able to benefit from the expertise of full-time professional fund managers without the need to worry about what kind of securities to buy and when to get in and out of the market. By investing in unit trust funds, you have the opportunity to spread your money over a diversified portfolio of assets which otherwise may not be possible on your own.In brief, the benefits you will get to enjoy with unit trust investment are:

Professional investment services

Diversification opportunities and minimised risks

Affordability

Convenience

Liquidity

Note: Any investment carries with it an element of risks. Therefore, prior to making an investment, prospective investors should consider the risk factors.

Thursday, January 05, 2006

The PRESENT

The Gift that Makes You Happy and Successful at Work and in Life.

by Spencer Johnson

The PRESENT is not the past and it is not the future. The PRESENT is the PRESENT moment. The PRESENT is now!

Saturday, December 31, 2005

The Financier QUOTES

There is nothing so comfortable as money, - but nothing so defiling if it be come by unworthily; nothing so comfortable, but nothing so noxious if the mind be allowed to dwell upon it constantly. If a man have enough, let him spend it freely. If he wants it, let him earn it honestly.

With money and wine, you will have many friends, but when you are in trouble, will you see even one?

When it comes to money, it's better to do nothing than to do something you don't understand.

The easier way for your children to learn about money is for you not to have any.

Anonymous

With money and wine, you will have many friends, but when you are in trouble, will you see even one?

Chinese proverd

When it comes to money, it's better to do nothing than to do something you don't understand.

Suze Orman

The easier way for your children to learn about money is for you not to have any.

Katharine Whitehorn

Happy New Year

Friday, August 05, 2005

Wealth Accumulation Insurance

Not all of us are born with a silver spoon. Many believe that low and moderate income families cannot afford to save and build wealth. Yet, everyone has the ability to accumulate wealth over time. Through contributions to a retirement program, education investments, and other savings during their working years, most can accumulate six-figure assets. Accumulating wealth is not a mystery. It simply takes time, patience and the following7 steps:

Not all of us are born with a silver spoon. Many believe that low and moderate income families cannot afford to save and build wealth. Yet, everyone has the ability to accumulate wealth over time. Through contributions to a retirement program, education investments, and other savings during their working years, most can accumulate six-figure assets. Accumulating wealth is not a mystery. It simply takes time, patience and the following7 steps:- Think long term and have realistic goals.

- Know your risk appetite.

- Start immediately.

- Invest systematically/regularly.

- Diversify your investments.

- Take advantage of tax reduction strategies.

- Stay on the course.

Monday, August 01, 2005

Mode of Investment

EPF

EPFThis allows you to invest part of your EPF Savings into our full range of unit trust funds. By investing some of your EPF Savings in a unit trust fund, you have the opportunity to achieve potentially higher returns on your savings over the long-term.

(a) How does it work?

- You must be below 55 years of age.

- You are only allowed to withdraw and invest 20% (at any one time) of the amount in excess of RM50,000 from your EPF Account 1, subject to a minimum investment of RM1,000. This means you must have at least RM55,000 saved in your EPF Account 1.

- Investments to a unit trust fund from your EPF Account 1 can only be made once every 3 months.

- Any income distributions paid by the unit trust fund will be considered as EPF savings and must be reinvested into additional units of the fund.

- You are redeeming your units in the unit trust fund, your redemption proceeds will be returned to your EPF Account 1.

Example:

Total Savings in Account 1

RM130,000

Required Balance in Account 1

RM50,000

Excess Amount

RM80,000

Investable Amount (20% x RM80,000)

RM16,000

Subsequent withdrawals can be made after 3 months from the last approved withdrawal.

(b) What do I do next?

Forward the following:

(b) What do I do next?

Forward the following:

- completed application form;

- photocopy of your identity card or passport duly thumb-printed; and

- completed KWSP 9F (AHL) (obtained from the EPF or from any of our offices) duly thumb-printed.

SAVINGS PLAN

Our Savings Plan allows you to invest smaller amounts on a regular basis. Though it may seem small at first, each month's contribution can develop into something quite substantial over time.

Our Savings Plan helps you to invest a fixed sum of money every month. This saves you the hassle of timing your investment. With a constant investment amount, you will buy more units when prices are low and fewer units when prices are high. This can work out to your advantage and is known as the Dollar Cost Averaging concept.

LUMP SUM

Under this option, you may invest at any time by cash in a lump sum, subject to the respective Funds' minimum initial investment and additional investment. You may invest a small lump sum, leave it to accumulate and assign amounts whenever you are able to invest.

Do's and Don'ts of Choosing a Unit Trust Fund

Do

- Decide which type of unit trust fund meets your saving needs.

- Shop around for a reliable unit trust company.

- Check whether investment limits, frequency of income payments, etc, are suitable.

- Check past performance records.

Don't

- Don't choose any unit trust fund just because its performance has been good, make sure it is the right fund for you.

- Don't pay too much attention to short term performance, good consistent performance over all periods is the best lead.

- Don't decide on a unit trust fund just because it has low charges, good performance is far more important.

- Don't borrow to invest in unit trust unless you are absolutely aware of the risk involved.

Saturday, July 30, 2005

Introduction to UNIT TRUST

The Basics (Introduction to unit trust)

The Basics (Introduction to unit trust)A unit trust fund is a collective investment scheme, which pools the savings of investors with similar investment objectives in a special "trust" fund managed by professional fund managers. The fund will then be invested in a diversified portfolio of equities, fixed income securities and other assets in accordance with the fund's investment objectives and as permitted under the SC's Guidelines on Unit Trust Funds. The organisation of a unit trust fund is a tripartite relationship between the manager, the trustee and the unitholders. The obligations and rights of each of the three parties are specified in the Deed, a legal document drawn up by the manager and registered with the SC. The Deed is designed to govern the operations of the trust fund and protect the unitholders' interests. The manager is responsible for the management and operations of the trust fund whilst the trustee holds all the assets of the fund.

Mode of Operation (Governed By The Deed)

Wednesday, July 06, 2005

Knowing what you are saving / investing for

All journeys have one thing in common, a destination...and here are some events in your life you may wish to save for:- Putting your child through private education.

- The wedding of your dreams.

- A new home.

- Your retirement.

Of course, you may not want to invest for any other reason than to make the most of your money. Unit trusts in general has a proven record over the long term to help you do just that.

Understanding risks and returns

Why investors should understand the meaning of risks? There is a direct relationship between risk and reward. A fundamental principle of investment is the risk reward trade-off associated with every investment decision made. The higher the risk, the greater the reward, but the reverse is also true! There are generally, three basic types of investment risk :

*General market risk that relates to a broad range of investments and is largely dependent on economic conditions and internal markets.

*Market sector risk that relates to a particular sector of a market, for example, financial stocks will perform better than plantation stocks at a particular period of time. This form of risk can be managed by carefully monitoring the economic scene with a view to identifying the winners and losers.

*Specific risks that relates to the performance of a particular security or property in an investment portfolio. For example, the performance of a specific company's share. The specific risk that one investment will not perform, over another can be minimised by carefully investigating and researching before buying and performing regular ongoing checks.

Since unit trusts invest in marketable securities, they are exposed to market environments. Fund managers seek to mitigate risks by building a broadly based portfolio.

Different types of funds involve different degrees of risk. Bond funds have historically proven to have less risk to capital than equity funds, since they are affected less by the fluctuations of the stock market. While equity investment can be more risky, it is more likely than a bond fund to provide long-term capital growth.

Benefits of Unit Trusts

*Access to markets and overseas opportunities. Unit trusts give you the opportunity to invest in specialised and/or overseas markets. Again, it would be difficult or impossible for an individual to access such markets directly due to limited capital resources as well as time required to be spent on careful research to gain in-depth knowledge of these markets.

*Low minimum investment. With as little as RM1,000, you can invest into a wide range of securities that you might otherwise not have access to. There are also regular savings plans which start from as low as RM100 so that you can continuously build on your investments.

*Professional management. Few of us are investment experts. The great thing about investing in unit trusts is that you leave your money in the hands of experienced professionals who devote their time to ongoing research and managing the funds.

*Spreading the risks. As a unit trust buys into a range of securities, the investment risk is reduced. This is because if any particular security proves to be a bad investment, the impact on such a diversified portfolio is not as significant as having put all eggs in one basket.

*Investments to cater to different objectives. There are many types of funds to meet a variety of financial objectives and an investor can use a portfolio of funds to achieve his or her objectives.

Investors would have different objectives when they invest. If you are planning to invest for your retirement 30 years later, you might consider using growth-oriented equity funds that have traditionally delivered healthy returns over a longer period. Other funds such as bond funds are suitable for those who prefer steady returns with lower risks.

Choosing the right fund for you

*What are your goals? Before you invest, determine your objectives and time horizon, and then balance them against the risks you are prepared to take. For example, if your goal is to accumulate wealth over a long period of time, your portfolio may comprise more equity funds than bond funds to focus on capital growth.

*What is your risk tolerance? It is not enough to want the highest returns on your investments as risks and returns go hand in hand. A high risk-taker would be prepared to weather a few knocks in exchange for the possibility of higher rewards. A more conservative investor would opt for steady but relatively lower returns and greater stability.

*Think medium to long-term. Most unit trusts offer potentially good returns over the long run. However, be prepared to hold onto your investments as unit trusts are regarded as medium to long-term investments

Just like many other investments, the value of unit trusts can rise and fall on a daily basis. But don't panic. If an investment temporarily falls, this can sometimes provide an excellent opportunity to invest more money, averaging your price when the market offers good value.

Tuesday, June 15, 2004

Thursday, October 10, 2002

ABOUT FINANCIAL PLANNING

People of Today - What Do They Want?

People of Today - What Do They Want?In today's fast growing economy, people are not only working towards financial growth and stability they are also looking towards a better lifestyle for themselves and their family. While chasing dreams of early retirement, sending their children for overseas tertiary education, owning a few units of properties and a diversified portfolio of investment instruments, many questions are left unanswered.

Often people have not taken sufficient steps to ensure that their assets are protected from risk as well as ensure that their dependants are adequately taken care of financially in the event they are no longer around or in active employment. While steps have been taken to ensure that there are some forms of assets distribution arrangements, the funds required during the interim period may not be adequately set aside or worse, these funds are not taken into consideration when making the arrangements.

Also, many of the people while investing their monies and receiving investment return had not been able to analyze the actual rate of return after inflation. In fact, their investment strategies may not be in-line with their Financial Goals and Objectives without them realizing it.

Realizing Financial Goals - What Do They Need?

How then can people fulfill their Financial Goals while maintaining their current lifestyle and make their savings work harder for them? What do people require in order to ensure that all aspects of achieving their Financial Goals are taken care of? When their life circumstance changes, how do they know what impact all these issues have on their existing strategies. What should they do?

The most talked about process today is Financial Planning. Although Financial Planning is relatively new to many people in Malaysia, it has been practiced in USA for more than 40 years. In Malaysia today, Financial Planning as a profession is regulated by the Securities Commission. Its importance and development stems from the recommendations in both the Capital Market Masterplan 2001 and Financial Sector Masterplan 2001.

Financial Planning - What is it all about?

Simply, Financial Planning is about helping an individual achieve his or her Financial Goals from where he or she is today. To many people, Financial Planning is a complicated process and that only the rich need to worry about it. Is this true? The answer is "No".

In fact, all of us need some form of Financial Planning. When we first purchase a house, we need to ascertain how much we can afford, how much loan to take, which financial institutions is giving the better rate and which loan is best suited to me for better cash flow management. When we invest our hard earned savings, we need to find out about our risk appetite, the time period of investment, the anticipated rate of return and asset portfolio.

If we need to categorize the different stages of the wealth management process and its solutions, it can be best described as follows:

1. Wealth Protection

- Insurance

2. Wealth Growth

- Unit Trust Funds

- Equities

- Properties

- Savings accounts etc

3. Wealth Creation

- Insurance

4. Wealth Distribution

- Wills

- Trust

Doing Financial Planning - What are the Benefits to Me?

1. Investment Growth Strategies for better Return on Investment.

2. Financial Protection in case of Disability and Critical Illness (when removed from Employment

Permanently or Temporary)

3. Health and Medical Coverage for Hospitalization and Surgical Costs

4. Safeguard Family Income to ensure Continuity of Lifestyle

5. Children's Tertiary Education especially for Overseas Education

6. Retirement Funds for Independent Post-Retirement Lifestyle

7. Emergency Funds for Contingency and Replacement Costs

8. Estate Distribution to ensure Proper Administration of Estate and Protection of Family's Assets

Financial Planning Process - What Do I Need to Know?

The Financial Planning Process involves a Six Step Process.

1. Establishing and Defining your Relationship with your Planner

2. Gathering of your Personal and Financial Data including Goals

3. Analyzing and Evaluating your Financial Status

4. Developing and Presenting Financial Planning Recommendations and/or alternatives

5. Implementing the Recommendations

6. Monitoring the Recommendations

Subscribe to:

Posts (Atom)

{kind=link}