- Save your money and get interest. Work to make money at the same time.

- Always have and work towards a financial goal. Adjust your goals as necessary but never abandon them.

- Begin a retirement and investment account now. The earlier you start a long term savings/investment account, the bigger the payoff in the future.

- If you don't have the CASH to pay for it, you can't afford it. Bring able to make the instalment payments doesn't mean you can afford it.

- Money isn't everything and greed is not good.

- Save at least 10% of each and every paycheque. Force yourself to do this. It will pay off in the LONG run.

- A sale in a store is not a sale if you can't afford it.

- Earn some, save some, spend some.

- Spend less than you earn.

- If your outflow exceeds your income, your upkeep will be downfall.

Monday, July 31, 2006

TOP 10 Money Rules

Saturday, July 01, 2006

June 2006 Market Review and Outlook

KLCI Continues to Ease with Regional Markets

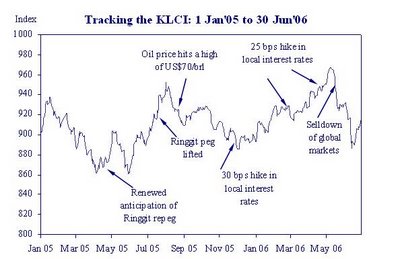

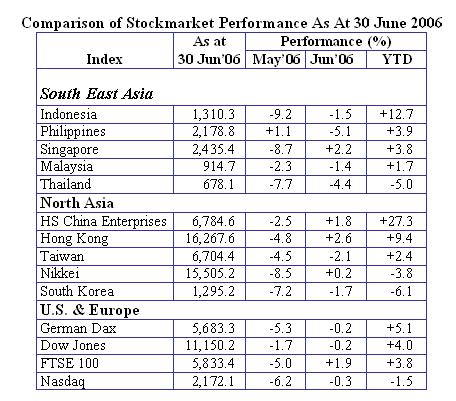

Commencing the month at 930.4 points, the KLCI fell amidst continued declines in regional markets to its year low of 883.2 points in mid-June. However, a rebound in global and regional markets towards the end of June helped the KLCI to close at 914.7 points for a reduced loss of 1.4% for the month of June 2006.

Regional markets closed on a mixed note as concerns of excessive tightening of U.S. monetary policy by the U.S. Federal Reserve diminished. A rebound on Wall Street caused selected regional markets to stem earlier losses in late June. South East Asian markets generally closed weaker while North Asian markets managed to register marginal gains in June.

On Wall Street, the Dow also eased to near its year low of 10,667.4 points in mid-June on concerns of further interest rate hikes before rebounding to 11,150.2 points, down by a marginal 0.2% for the month. The Nasdaq closed 0.3% lower at 2,172.1 points over the same period.

Commencing the month at 930.4 points, the KLCI fell amidst continued declines in regional markets to its year low of 883.2 points in mid-June. However, a rebound in global and regional markets towards the end of June helped the KLCI to close at 914.7 points for a reduced loss of 1.4% for the month of June 2006.

Regional markets closed on a mixed note as concerns of excessive tightening of U.S. monetary policy by the U.S. Federal Reserve diminished. A rebound on Wall Street caused selected regional markets to stem earlier losses in late June. South East Asian markets generally closed weaker while North Asian markets managed to register marginal gains in June.

On Wall Street, the Dow also eased to near its year low of 10,667.4 points in mid-June on concerns of further interest rate hikes before rebounding to 11,150.2 points, down by a marginal 0.2% for the month. The Nasdaq closed 0.3% lower at 2,172.1 points over the same period.

Malaysia’s export growth slowed to a 9-month low of 6.3% in April from 9.5% in March and 11.9% in 1Q2006 due to slower exports of electronic & electrical and commodity products. Likewise, import growth also eased to 11.4% in April from 14% in March on weaker imports of capital and consumption goods. As a result, Malaysia’s trade surplus narrowed to RM7.2bil in April from RM9.6bil in March. The cumulative trade surplus for the January to April 2006 period of RM33 bil is about the same level as the previous corresponding period in 2005.

Malaysia’s export growth slowed to a 9-month low of 6.3% in April from 9.5% in March and 11.9% in 1Q2006 due to slower exports of electronic & electrical and commodity products. Likewise, import growth also eased to 11.4% in April from 14% in March on weaker imports of capital and consumption goods. As a result, Malaysia’s trade surplus narrowed to RM7.2bil in April from RM9.6bil in March. The cumulative trade surplus for the January to April 2006 period of RM33 bil is about the same level as the previous corresponding period in 2005.Domestic demand remained resilient with consumer loans growth moderating slightly to 17% in May from 18.6% in April as demand for vehicle financing weakened amid uncertainty over the outlook for car prices. The banking system’s overall loans growth remained stable at 8.9% in May on the back of firm demand for corporate loans.

Malaysia’s foreign reserves rose by a bigger margin of RM10.5bil in May to RM289.5bil as at 31st May compared to an increase of RM7.4bil in April. The increase in reserves is attributable to higher repatriation of export earnings and net capital inflows.

The local inflation rate eased to 3.9% in May from 4.6% in April as transport costs rose at a slower pace of 12.4% in May compared to 16.9% in April. However, the inflation rate is expected to remain high in coming months following Tenaga’s hike in electricity rates with effect from 1st June.

On the international front, economic activities in the U.S. show signs of moderating with the U.S. durables goods order growing at the slowest pace in 10 months of 3.3% in May from 10.8% in April following a sharp fall in civilian aircraft orders. However, consumer confidence as measured by the Conference Board rebounded slightly to 105.7 in June from 104.7 in May due to expectations that the business outlook and the job market are likely to improve.

The U.S. inflation rate rose to a 7-month high of 4.2% in May from 3.5% in April due mainly to higher fuel prices while core inflation (excluding food and energy) edged up to a 15-month high of 2.4% from 2.3% over the same period.

The Federal Reserve raised the Federal funds rate for the 17th time by 25 basis points to a 5-year high of 5.25% at the FOMC meeting on 29th June. Although the Federal Reserve stated that economic growth is moderating from its strong pace earlier this year, it noted that some inflationary risks remain and the outlook for interest rate policy will depend on the incoming data.

On the currency front, the U.S. dollar strengthened by 2.8% against the Euro and 4% against the Yen respectively in June on expectations that U.S. interest rates will continue to exceed interest rates in Europe and Japan. The U.S. dollar also appreciated versus other regional currencies amid the recent correction in emerging markets. The Ringgit eased by 1.5% to RM3.69 against the U.S. dollar for the month. Meanwhile, oil prices moved in a trading range around the US$70/brl level in June before ending the month unchanged at US$71/brl.

Stockmarket Outlook

The sharp correction in global and regional financial markets in May and June was triggered by concerns that an overtightening of U.S. monetary policy by the U.S. Federal Reserve could lead to a sharper-than-expected slowdown in the global economy. After making 17th consecutive hikes in interest rates, the U.S. Federal Reserve may be reaching the end of its monetary tightening cycle with a potential pause in interest rates after another potential hike at the 8th August FOMC meeting.

Despite concerns over the effect of tighter monetary policies, global economic growth is still expected to be sustained at between 4% and 5.0% this year compared to 4.8% last year. The anticipated slowdown in U.S. economic growth could be mitigated by the current strengthening of the Japanese and Euroland economies while China continues to grow at a strong pace.

On the regional front, economic growth is expected to moderate in most Asian economies in 2H2006 as global demand for manufactured exports weakens in tandem with the anticipated slowdown in the U.S. economy. However, selected regional economies with a significant domestic sector may be able to mitigate any slowdown in the external environment. On the valuations front, the recent sell-down in regional markets has sufficiently discounted the risk of overtightening by the U.S. Federal Reserve as valuations of selected regional markets have reached fairly attractive levels.

On the local front, Bank Negara is expected to maintain a tightening stance on monetary policy to keep inflationary pressures under control and ensure that real interest rates remain positive. However, the anticipated hikes in domestic interest rates in 2H2006 are expected to be moderate given the prospect of a peaking in U.S. interest rates by August 2006 and the high levels of liquidity in the banking system.

Despite the challenging external environment, Bursa Securities is a defensive market underpinned by fair valuations and reasonably attractive dividend yields. Bursa Securities’ P/E rating of 14.7x 2006 earnings is 17% below the 7-year historical average (1999-2005) of 17.7x. The market is underpinned by a gross dividend yield of 4.5% which compares favorably to Ringgit fixed deposit rates for less than a year’s tenure.

Subscribe to:

Posts (Atom)